Introduction

Traditional insurance underwriting runs on manual document review, scattered data sources, and judgment calls that stretch decision cycles into days or weeks. Pricing errors slip through. Fraud signals go unnoticed. Faster competitors win the risks worth writing.

The numbers behind this are hard to ignore: approximately 40% of an underwriter's time disappears into administrative work rather than actual risk evaluation, and most carriers quote only 50% of their commercial submissions because they simply can't process opportunities fast enough.

This article walks through how AI underwriting works, how it automates every step from application intake through policy issuance, the measurable benefits carriers are seeing, real-world applications across insurance lines, the honest implementation challenges, and a practical starting point for adoption.

TLDR:

- AI compresses standard underwriting cycles from days to minutes

- ML models evaluate hundreds of risk signals — versus the traditional 5-10 — improving accuracy and loss ratios

- Proven use cases span P&C, life & health, and commercial/specialty lines

- Bias, compliance, and data quality must be resolved before production deployment

What Is AI in Insurance Underwriting?

AI underwriting applies machine learning algorithms, natural language processing, predictive analytics, and automation to evaluate applicant risk, set coverage terms, and issue policy decisions—mostly without manual intervention for standard cases. Where traditional processes rely on underwriters manually pulling data from credit bureaus, inspection reports, and claims databases, then applying static rule sets with incomplete information, AI systems aggregate data automatically, recognize complex patterns across hundreds of variables, and generate consistent decisions at scale.

Current adoption sits at 14% but is projected to hit 70% within three years, based on a survey of 430 senior underwriting executives across 11 countries. Lloyd's market saw AI adoption more than double in 12 months, with 93% of participating firms building formal AI governance frameworks.

In practice, AI handles the routine heavy lifting so underwriters can focus where judgment matters most:

- Aggregates data from credit bureaus, claims histories, and inspection reports automatically

- Recognizes risk patterns across hundreds of variables simultaneously

- Processes standard risks end-to-end without manual touchpoints

Human underwriters remain essential for complex, high-value, or ambiguous cases. The technology augments expertise rather than replacing it — underwriters shift toward strategic analysis, exception handling, and client relationships, away from administrative grind.

How AI Automates the Insurance Underwriting Workflow

Application Intake and Automated Data Prefill

AI uses NLP and optical character recognition to extract structured data from unstructured application documents—forms, inspection reports, broker submissions—then cross-references public records, third-party data providers, and historical claims databases to prefill fields automatically. This eliminates manual data entry and the errors that come with it.

NLP and computer vision achieve 92-94% extraction accuracy for insurance-specific entities in submission ingestion. QBE Insurance Group now processes 100% of broker submissions using AI-powered solutions.

Automated triage routes standard submissions toward straight-through processing while flagging complex or anomalous applications for human review—improving throughput without sacrificing oversight.

Risk Assessment and Predictive Scoring

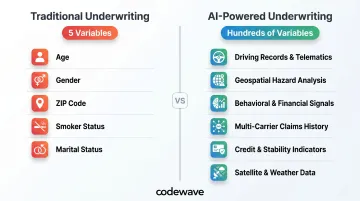

Machine learning models replace static rating tables with dynamic risk scores. Instead of the 5 criteria traditional life insurers typically use (age, gender, ZIP code, smoker status, marital status), AI models draw on hundreds of variables:

- Driving records and telematics data

- Geospatial and property-level hazard analysis

- Behavioral signals from social and financial data

- Claims history across multiple carriers

- Credit profiles and financial stability indicators

- Satellite imagery and weather pattern data for property risks

These models continuously update as new claims data flows in, so risk scores reflect current loss experience rather than outdated actuarial assumptions frozen in annual rate filings.

Policy Decisioning and Pricing

AI translates risk scores into coverage recommendations and premium calculations by applying carrier appetite rules, regulatory constraints, and profitability targets simultaneously. The output is decision-ready—approve, decline, or refer—along with suggested policy terms and pricing structured around three outputs:

- Coverage recommendation: approve, decline, or refer to a specialist

- Pricing: premium calculated against real-time risk score and profitability targets

- Policy terms: conditions adjusted to carrier appetite and regulatory constraints

Unlike human judgment, which varies between underwriters handling similar risks, AI applies these rules uniformly across every submission—reducing decision variance and improving portfolio quality.

Fraud Detection

Anomaly detection models flag inconsistencies before a policy issues:

- Mismatches between stated and third-party information

- Submission patterns that mirror known fraud schemes

- Unusual claim histories or application timing

Total insurance fraud costs businesses and consumers $308.6 billion annually, with life insurance fraud at $74.7 billion and P&C fraud at $45 billion. A European insurer using AI-driven fraud detection shaved up to 5 points from the combined ratio, generating 3X the expected volume of relevant policy alerts.

Catching fraud at underwriting rather than claims prevents losses that would otherwise hit the combined ratio before they're written into the book.

Portfolio Monitoring and Renewal

AI continuously monitors portfolio concentration, loss development, and external risk factors—weather events, economic indicators, regulatory changes—to surface accumulation risks and trigger proactive renewal adjustments. Portfolio management moves from an annual retrospective to an ongoing discipline—one that responds to emerging exposures as they develop, not after losses materialize.

On the policy level, AI enables scheduled alerts at new business, claims, and pre-renewal stages, with daily analysis during the "free look" period to identify risk before policies are fully bound.

Key Benefits of AI-Powered Risk Assessment and Policy Decisioning

Speed

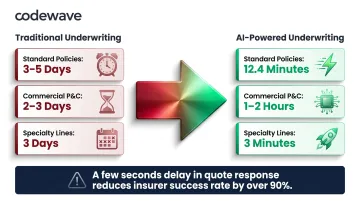

AI reduced average underwriting decision time from 3-5 days to 12.4 minutes for standard policies, maintaining 99.3% accuracy. Commercial and specialty P&C decisions that traditionally took 2-3 days now take 1-2 hours. Hiscox achieved a 99.4% reduction in cycle time for London Market specialty lines—from 3 days to 3 minutes.

That speed translates directly to revenue. A delay of only a few seconds in quote response reduces an insurer's success rate by over 90%, with a clear correlation between response time and quote-to-bind conversion rates.

Accuracy and Loss Ratio Improvement

Better speed means little without better decisions. AI models trained on large, diverse datasets identify risk patterns humans cannot, producing a 43% improvement in risk assessment accuracy for complex policies. That precision flows directly to the bottom line: commercial P&C insurers using agentic AI see a 3-5 percentage point improvement in loss ratios. On a $1 billion premium portfolio, a 4-point gain means $40 million in annual underwriting profit.

Cost Reduction

Automating routine underwriting tasks cuts costs at every layer — fewer manual touchpoints, less rework from data errors, and lower referral rates. McKinsey estimates gen AI could unlock $50-70 billion of value for the insurance industry, with Accenture projecting up to 30% productivity gains in underwriting roles and up to 65% of working hours subject to automation or augmentation.

Real-world results back this up. N2G Worldwide achieved a 40% increase in underwriter quote capacity and a 60% reduction in cycle times after deploying AI-driven automation.

Fraud Risk Mitigation

Early-cycle fraud detection prevents losses that would otherwise reach the claims stage, directly improving combined ratios. The FBI estimates fraud costs the average U.S. family $400-$700 annually in increased premiums. Catching fraud before policy issuance rather than at claims protects both the carrier's combined ratio and policyholders' premium rates.

Personalized Pricing and Customer Experience

Granular risk scoring enables micro-segmented pricing. Applicants with genuinely low risk pay less, while the carrier maintains adequate margin on higher-risk segments. Carriers using AI-driven risk scoring report 10-15% growth in new business premiums and 5-10% gains in broker retention — a measurable edge in both acquisition and retention.

AI Use Cases Across Insurance Lines

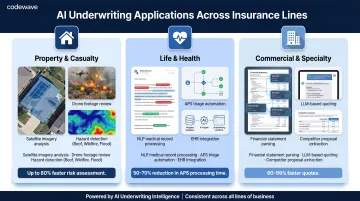

Property and Casualty Insurance

AI analyzes satellite imagery, drone footage, weather data, and property inspection records to assess structural risk remotely—reducing the cost and latency of physical inspections while improving hazard detection accuracy for home, auto, and commercial property lines.

Only approximately 30% of insurers currently use geospatial and location intelligence in underwriting. Higher-resolution imagery supports property-level risk scoring at scale, replacing static snapshots with continuous monitoring. Multimodal AI models can analyze thousands of satellite and social media images for hazard detection, flagging:

- Roof condition and structural vulnerabilities

- Vegetation proximity and wildfire exposure

- Nearby flood risks and drainage patterns

- Hazards invisible to traditional underwriting methods

Life and Health Insurance

Traditional life underwriting takes 4-6 weeks, requiring review of medical records, driving records, and medical exam results. Attending Physician Statement (APS) files often consist of hundreds or thousands of scanned pages per applicant.

NLP models process unstructured medical records, lab results, and prescription histories within minutes or seconds—allowing underwriters to search key sections instantly rather than reading start to finish. Triage models auto-tag likely declines for routing to junior underwriters, cutting APS review time significantly.

52% of life insurance executives expect Electronic Health Records (EHRs) to have the greatest impact on underwriting speed over the next 3-5 years, with 57% identifying younger consumers' demand for faster, digital-first experiences as a key transformation driver.

Commercial and Specialty Lines

Commercial underwriting—cyber, D&O, E&O, marine—involves diverse, complex, unstructured risk data. AI parses financial statements, news feeds, regulatory filings, and industry loss data to build a more complete risk picture than a human reviewer working under time pressure.

Agentic AI achieves 60-99% faster quotes for commercial P&C insurers. AmTrust implemented an LLM-based quoting platform that extracts data from competitor proposals to generate bindable quotes automatically. These systems learn from decision patterns, surface portfolio-level insights, and proactively guide underwriters toward strategic opportunities. Underwriting teams handle higher submission volumes without proportional headcount growth.

That capacity to scale is reflected in broader market growth. US premium volumes through MGAs grew 14% annually over the last decade, from $47 billion in 2020 to $97 billion in 2024—driven partly by technology-enabled distribution models that depend on automated underwriting at their core.

Challenges and Ethical Considerations of AI Underwriting

Algorithmic Bias and Fairness

AI models trained on historical underwriting data risk encoding the biases embedded in past decisions—discriminating against certain ZIP codes, demographics, or professions in ways that are both ethically problematic and potentially illegal.

California Insurance Commissioner issued Bulletin 2022-5 addressing racial bias and unfair discrimination. Colorado SB21-169 requires insurers to test their big data systems—including external consumer data, algorithms, and predictive models—for unfair discrimination. Documented problem areas include:

- ZIP code-based SIU flagging that proxies for race or income

- Biometric data bias from facial recognition inputs

- Algorithmic proxy discrimination through seemingly neutral variables

Carriers need diverse training data, regular bias audits, and human review checkpoints to prevent discriminatory outcomes. Regulation has followed—precisely because voluntary controls alone haven't been sufficient.

Regulatory Compliance and Explainability

The NAIC Model Bulletin on AI, adopted December 2023, establishes guidelines for responsible AI use across the insurance lifecycle. As of March 2025, 24 states have adopted the bulletin. Key requirements:

- Written AI program with governance framework

- Cross-functional representation (legal, compliance, underwriting, data science, actuarial)

- Consumer notice of AI use

- Risk controls addressing data quality and bias

- Third-party vendor management with audit rights

EIOPA classified AI systems used for risk assessment and pricing in life and health insurance as high-risk under the EU AI Act, requiring transparency, data governance, and human oversight.

The explainability challenge is real. Insurers must articulate why an AI system denied or priced a policy, which is difficult with black-box models. Carriers need model documentation, audit trails, and interpretable frameworks — think SHAP values, LIME explanations, or plain-language reason codes that satisfy adverse action notice requirements.

Data Privacy and Security

AI underwriting systems ingest sensitive personal and financial data at scale, creating serious privacy obligations. A Lloyd's market survey identified data privacy, cybersecurity, and third-party risk as leading AI concerns, with over 60% of firms mandating human oversight of AI-generated outputs.

Carriers must ensure data handling complies with applicable regulations and that model inputs don't include impermissible rating factors.

How Insurance Carriers Can Get Started with AI Underwriting

Assess Data Readiness First

AI underwriting systems are only as good as the data feeding them. Carriers should audit their data for completeness, historical depth, and labeling quality before selecting or building models. Poor data quality produces biased, inaccurate outputs regardless of model sophistication.

According to Accenture's Underwriting Rewritten report, data maturity varies sharply across lines:

- 44% of underwriting divisions make extensive use of synthetic data; 38% rely heavily on structured data

- Structured data use in Commercial P&C: 63%; Personal/Retail P&C: 69%; Life insurance: only 12%

- Data-gathering and cleansing solutions sit at 33% adoption today, projected to reach 85% within three years

That gap between current adoption and near-term projections signals where carriers need to invest before anything else.

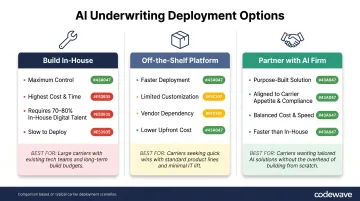

Decide on Build vs. Buy vs. Partner

Three paths exist for deploying AI underwriting capabilities:

- Build proprietary models in-house — Maximum control, high cost and time, requires 70-80% in-house digital talent

- Adopt off-the-shelf insurtech platforms — Faster deployment, less customization, vendor dependency

- Partner with an AI development firm — Purpose-built solutions tailored to carrier appetite, data architecture, and compliance requirements

For carriers that want custom solutions aligned with their specific underwriting appetite and regulatory environment, working with a partner like Codewave—which has built AI and automation solutions across insurance and 15+ industries—can speed up implementation while reducing risk compared to building from scratch.

Start with a Bounded Use Case, Then Scale

Begin with a single, high-volume, lower-complexity underwriting workflow—personal auto or homeowners—to prove out the model, measure performance, and build organizational confidence before expanding to more complex lines. This limits exposure, surfaces ROI early, and gives teams room to refine the model based on actual underwriting outcomes before scaling.

Frequently Asked Questions

What is underwriting AI?

Underwriting AI refers to the use of machine learning and predictive analytics to automate risk evaluation, pricing, and policy decisioning in insurance. It enables faster, more consistent decisions than traditional manual underwriting by analyzing hundreds of risk variables at once.

Can AI be used in underwriting?

Yes, AI is actively used across all major insurance lines today. It handles data extraction, risk scoring, fraud flagging, and straight-through processing for standard policies. Human underwriters retain oversight for complex or high-value risks, focusing on exception handling and strategic analysis.

What are the three types of underwriting?

The three main types are:

- Insurance underwriting — assessing policyholder risk

- Securities underwriting — evaluating financial instruments for public offering

- Loan/mortgage underwriting — assessing borrower creditworthiness

This article covers insurance underwriting specifically.

Will AI replace human insurance underwriters?

No. AI automates routine and data-heavy underwriting tasks but does not replace human judgment. Underwriters shift toward higher-value work — complex risk analysis, exception handling, relationship management, and portfolio strategy — with AI handling the volume so underwriters focus on the decisions that actually require expertise.

How does AI detect fraud in insurance underwriting?

AI uses anomaly detection to cross-reference application data against third-party sources, flag inconsistencies, and identify submission patterns that match known fraud profiles. This catches fraudulent applications before a policy is issued rather than at the claims stage, protecting the combined ratio by reducing loss exposure before it occurs.

What are the main challenges of implementing AI in underwriting?

Three challenges come up consistently:

- Data quality and bias — models trained on flawed historical data reproduce past errors at scale

- Regulatory explainability — carriers must justify AI decisions to regulators and consumers in plain terms

- Change management — getting underwriters to trust and act on AI recommendations takes deliberate effort