Introduction

Finance teams face constant pressure from manual, repetitive tasks: data entry, invoice matching, bank reconciliations, and compliance checks consume hours daily. These workflows drain resources, slow processing times, and inflate operating costs — leaving teams little capacity for strategic analysis.

According to Grand View Research, the RPA market in banking and financial services is projected to reach $8.79 billion by 2030, growing at a 39.4% CAGR. Finance leaders across fintech, insurance, and enterprise banking are moving automation from the pilot stage to core operations.

This article covers the highest-impact RPA use cases in finance — invoice processing, bank reconciliation, financial close, fraud monitoring, customer onboarding, and tax reporting — with cost and time benchmarks, and practical guidance for teams ready to deploy.

TLDR

- RPA deploys software bots to execute rule-based finance tasks like logging in, validating entries, and routing approvals—no human intervention required

- Highest-impact use cases: invoice processing, bank reconciliation, financial close, fraud monitoring, customer onboarding, and tax compliance

- Typical outcomes: 78% lower invoice processing costs, 30-50% faster close cycles, and screening automation that cuts into the $206.1B global compliance burden

- Start with high-volume, rule-based processes that have clear before/after metrics—not everything at once

- RPA handles structured tasks; AI extends automation to unstructured data and judgment workflows—use both together

What Is RPA in Finance and Why Are Finance Teams Adopting It?

RPA in finance is software that mimics human actions to execute structured, rule-based tasks without manual intervention. Typical actions include:

- Logging into systems and extracting invoice data

- Validating ledger entries and reconciling accounts

- Routing approvals and posting transactions

Unlike AI, which learns and adapts, RPA bots follow fixed rules and predefined workflows. They don't interpret context or make judgment calls — they replicate the exact steps a human would take across existing systems, just faster and without fatigue.

Finance teams are under mounting pressure: faster close cycles, tighter compliance requirements, surging transaction volumes, and frozen headcount are forcing leaders to automate routine work to free up capacity for strategic work. Gartner's 2025 AI in Finance Survey found that 59% of finance functions now use AI or automation—up from 37% in 2023—with accounts payable process automation the second most common use case at 37% adoption.

The numbers back that shift. The BFSI RPA market was valued at $685.7 million in 2022 and is growing at a 39.4% CAGR toward $8.79 billion by 2030. KYC compliance alone costs U.S. banks with $10 billion or more in assets an average of $50 million annually. Manual invoice processing runs $12.88 per invoice versus $2.78 for best-in-class automated teams — a 78% cost gap that compounds fast at scale.

Top RPA Use Cases in Finance That Reduce Costs and Speed Up Processing

RPA delivers the highest ROI in processes that are high-volume, rule-based, and prone to human error. The six use cases below meet all three criteria and represent the most proven automation opportunities in finance.

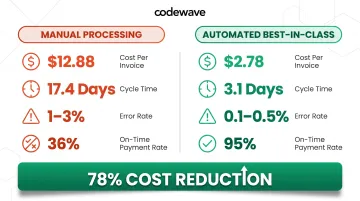

Invoice Processing and Accounts Payable Automation

RPA bots capture invoice data using OCR, validate it against purchase orders, code it to the correct general ledger accounts, route it for approval workflows, and post it to ERP systems—eliminating manual data entry at every step. This is the most common starting point for finance RPA because time-savings metrics are measurable and immediate.

Cost and cycle time impact:

| Metric | Manual Processing | Automated (Best-in-Class) |

|---|---|---|

| Cost per invoice | $12.88 | $2.78 |

| Processing cycle time | 17.4 days | 3.1 days |

| Error rate | 1-3% per data point | 0.1-0.5% |

| On-time payment rate | 36% | 95% |

Source: Aberdeen Group / Quadient benchmarks via Gennai

A company processing 1,500 invoices monthly at $12.88 each spends approximately $231,840 annually. Automation at $2.78 per invoice cuts that to roughly $50,040—a direct savings of $181,800.

Beyond hard costs, 55% of all B2B invoiced sales in the U.S. are overdue, with suppliers waiting an average of 43 days for payment and incurring $39,406 annually in late-payment-related expenses. Faster AP cycles reduce late-payment penalties, strengthen vendor relationships, and free staff from data entry for higher-value work.

Bank Reconciliation

RPA automates the matching of ledger entries against bank statements by pulling data from multiple accounts, applying matching rules (date, amount, reference number), flagging discrepancies, and routing exceptions to human reviewers. This eliminates the most time-consuming parts of a task that previously consumed hours of analyst time each cycle.

APQC benchmarking data shows that top-quartile organizations reconcile the general ledger in 5 hours, while bottom-quartile performers take 10 hours—a 100% gap driven by multiple systems, missing transactions, and manual document tracing. Separate estimates suggest cash reconciliation specifically consumes 20-50 hours per month for most teams using 3-5 systems.

Speed aside, accuracy matters just as much here: bots apply matching rules consistently across every transaction, reducing the risk of undetected discrepancies that cause audit complications or financial restatements. Manual reconciliation is vulnerable to fatigue, distraction, and inconsistent judgment—bots are not.

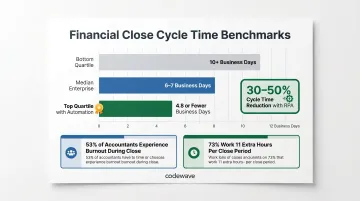

Financial Reporting and Period Close

RPA automates recurring journal entries, inter-company data consolidation, and report population during month-end and quarter-end close—compressing a multi-day process into hours by removing the manual steps of pulling, formatting, and moving data between systems.

Close cycle benchmarks:

- Median financial close: 6-7 business days for mid-to-large enterprises

- Top-quartile performers: 4.8 business days or fewer

- Automation impact: 30-50% cycle time reduction (BlackLine and Ventana Research)

- Manual reconciliation burden: Consumes 30-40% of total close cycle time

Source: APQC / BPR Global

Finance teams using RPA for close reporting spend less time on mechanics—chasing information from other departments, manually consolidating spreadsheets, correcting data entry errors—and more time on variance analysis and commentary. This directly improves the quality and timeliness of financial insights delivered to leadership. Separately, 53% of accountants experience burnout during the close, and 73% work an average of 11 extra hours per close period—automation addresses both productivity and retention.

Fraud Detection and AML Compliance Monitoring

RPA bots monitor transaction streams in real time, cross-check payment details against fraud and sanctions databases, apply anti-money laundering rule sets, and surface suspicious patterns for analyst review. This dramatically increases screening throughput compared to manual review—one global bank reduced alert investigation time from approximately 4 hours per alert to seconds using AI-powered automation modules.

LexisNexis Risk Solutions found financial institutions bear $206.1 billion in annual financial crime compliance costs globally, with labor costs ranking highest in overall spending. RPA-driven screening automation directly attacks that largest cost component. Global AML fines totaled $4.6 billion in 2024, with North America accounting for 94% of global penalties.

Consistent rule application and automated audit trails reduce regulatory exposure and support faster investigation workflows. Bots don't get fatigued or skip steps during high-volume periods—they apply the same screening logic to transaction 1 and transaction 10,000.

Customer Onboarding and KYC

RPA accelerates Know Your Customer procedures by extracting data from submitted documents, running automated identity checks against watchlists and registries, populating account systems, and triggering welcome workflows. This reduces onboarding time from days to hours without sacrificing compliance accuracy.

Fenergo's 2025 global study found 70% of financial institutions lost clients over the past year due to slow onboarding—the highest rate ever recorded—and the average annual spend on AML/KYC operations reached $72.9 million per firm globally. UK corporate bank onboarding often exceeds six weeks, and the global average customer abandonment rate stands at 10%.

Faster onboarding improves customer satisfaction, reduces the cost per new account, and directly protects revenue at scale for banks and fintech platforms. For high-volume institutions, shaving even one week from onboarding across thousands of accounts each year translates directly to measurable revenue retention.

Tax Reporting and Regulatory Compliance

RPA automates data collection from finance and tax systems, classifies transactions for tax purposes, reformats trial balances, and populates filing templates. This reduces the manual effort that makes tax season a bottleneck and lowers the risk of filing errors that trigger audits or penalties.

A Forrester Total Economic Impact study for Thomson Reuters found that a composite organization completing 500 tax returns annually loses more than 10,000 hours to manual tax processes. Automation delivered a 50% reduction in tax preparation time, 148% ROI, and $1.7 million in NPV over three years. The study also identified $667,000 in avoided compliance and remediation costs, including penalties and rework.

Bots can also monitor regulatory feeds and alert stakeholders when relevant rule changes are published, giving compliance teams a head start rather than a scramble. The IRS assesses a failure-to-file penalty of 5% of the tax due for each month or partial month a return is late—automation directly reduces this exposure.

The Real Cost and Time Savings From RPA in Finance

Industry-validated benchmarks show RPA delivers measurable returns across finance operations:

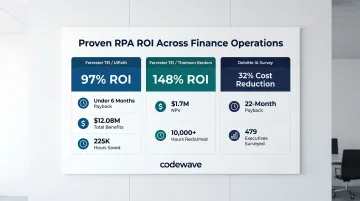

ROI benchmarks:

| Source | ROI | Payback Period | Key Metric |

|---|---|---|---|

| Forrester TEI / UiPath | 97% (3-year) | Less than 6 months | $12.08M total benefits; 225K hours saved in Year 3 |

| Forrester TEI / Thomson Reuters | 148% | Not specified | $1.7M NPV; 10K+ hours reclaimed |

| Deloitte IA Survey | 32% avg cost reduction | 22 months avg | 479 executives, 35 countries |

Codewave's tracked client outcomes provide concrete proof points: 50% faster invoice processing, 90% fewer data errors, 25% reduction in costs, 40% increase in productivity, and 40% less reporting time—achievable benchmarks when RPA is implemented with outcome accountability.

These savings compound from four cost levers:

- Fewer manual labor hours on routine tasks

- Lower error-correction and rework costs

- Reduced late-payment penalties

- Avoided compliance fines (labor is the largest AML cost component)

For a mid-sized finance operation processing 18,000 invoices annually, the shift from $12.88 to $2.78 per invoice alone saves approximately $181,800. Add reconciliation time savings (5-10 hours per cycle) and close compression (1-3 days per period), and the business case builds quickly.

Short-Term vs. Long-Term ROI

Early gains come from time savings on specific processes: invoice processing drops from 17 days to 3 days, reconciliation shrinks from 10 hours to 5 hours. These wins are measurable within the first quarter of deployment.

Longer-term gains come from scalability. Bots handle volume spikes—month-end, tax season, year-end close—without adding headcount, overtime costs, or temporary staffing. Operating 24/7 without fatigue, they directly address the peak-period strain that strains most finance teams.

How to Implement RPA in Finance: Where to Start

Start small, prove value, then scale. Identify two or three high-volume, rule-based processes with clear before/after metrics—invoice processing time, reconciliation hours per cycle, close cycle days—automate those first, measure outcomes, then use results to build internal buy-in for broader rollout.

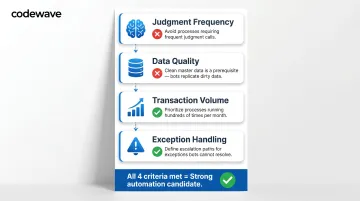

Process readiness checklist:

Before automating, apply these four criteria:

- Processes requiring frequent judgment calls or significant variation by transaction are not automation-ready

- Dirty master data—inconsistent vendor records, mismatched chart of accounts—gets replicated faster by bots, not fixed; clean data is a prerequisite

- Processes running fewer than a few hundred times per month deliver minimal ROI; prioritize high-frequency, repetitive tasks

- Every automated process needs a defined escalation path for exceptions bots can't resolve

Processes that pass all four criteria are strong automation candidates.

Two operational requirements should be in place before the first bot goes live:

Data quality: Bots executing against inconsistent vendor master records or duplicate chart-of-accounts entries will compound errors, not fix them. If your AP team regularly corrects vendor data or researches coding discrepancies, resolve those root issues first.

Central governance: Scattered bots with no clear owner become a maintenance problem fast. Assign a bot owner, set a monitoring cadence, and document the update process from day one. Bots that ran flawlessly at launch can fail silently when an upstream system changes its export format or a new approval threshold is introduced.

RPA vs. AI in Finance: Will AI Replace RPA?

RPA and AI serve different roles: RPA excels at high-volume, structured, rule-based tasks with predictable inputs—invoice matching, journal entry posting, reconciliation matching. AI and agentic automation handle unstructured data, contextual judgment, and multi-step decision workflows—anomaly detection, contract interpretation, regulatory research. Used together, they cover far more ground than either can alone.

That combination is already showing up in production environments. Common convergence patterns include:

- Intelligent document processing — RPA's execution speed paired with AI's ability to interpret unstructured invoices or receipts

- Anomaly detection — machine learning layered on RPA-driven transaction monitoring to flag patterns a rules engine would miss

- Predictive cash flow analysis — AI handles forecasting while RPA manages data collection and report distribution

According to Thomson Reuters, RPA is "process-driven" and follows predefined instructions without learning, while AI agents are "goal-oriented," leveraging generative AI and LLMs to adapt to changing situations and improve outputs. For finance leaders, the practical path is to start with pure RPA for the highest-volume rule-based tasks—AP, reconciliation, close automation. Then layer in AI for use cases requiring interpretation or judgment, rather than waiting for a fully AI-native solution before automating anything.

Gartner's 2025 survey confirms that error and anomaly detection is the third most common AI use case in finance at 34% adoption. Yet 91% of respondents report only "low or moderate" impact during early AI stages, and 25% are still uncertain how to move from planning to piloting. Rule-based RPA remains the practical starting point — with AI augmentation added as organizations build maturity and confidence.

Frequently Asked Questions

What is RPA in finance?

RPA is software that automates structured, repetitive finance tasks by mimicking human actions across existing systems—logging in, extracting data, validating entries, routing approvals, and posting transactions. Common examples include invoice processing, account reconciliation, and close reporting.

How is RPA used in finance?

RPA is deployed across AP/AR, reconciliation, financial reporting, compliance monitoring, fraud detection, and customer onboarding. Bots handle data extraction, validation, routing, and posting without human intervention, freeing teams for strategic analysis.

How do you implement RPA in finance?

Start by identifying high-volume, rule-based processes with clear performance baselines. Run a controlled pilot, measure outcomes, then scale with governance structures covering bot ownership and change management.

Will AI replace RPA in finance?

No. AI and RPA are complementary—RPA handles structured, rule-based tasks while AI extends automation to unstructured data and complex decisions. Most finance teams run both in tandem: bots execute the transactional work while AI handles interpretation, exception flagging, and judgment calls.

What are the leading RPA software tools for financial services?

The most widely adopted platforms are UiPath, Microsoft Power Automate, Automation Anywhere, and SS&C Blue Prism — UiPath and SS&C Blue Prism were named Leaders in the 2024 Gartner Magic Quadrant for RPA for the sixth consecutive year. Choose based on your integration requirements, process complexity, and scalability needs.